Amidst continued volatility in the global economic and industrial landscape, the market is re-evaluating the relationship between risk, policy, and liquidity. Over the past period, geopolitical frictions, trade disputes, technological competition, supply chain restructuring, and capital market fluctuations have collectively created a highly uncertain landscape.

Previously, Chen Rui, co-founder and chief strategy officer of SHINDEV, proposed that Sino-US relations are gradually shifting from highly uncertain confrontational expectations to a new stage that places greater emphasis on risk management, competitive boundaries, and pragmatic communication. In the view of the SHINDEV team, this judgment applies not only to international relations but also serves as a key to understanding current market recovery signals, changes in liquidity expectations, and the reassessment of industrial opportunities.

Of course, the market has not completely emerged from the fog. The International Monetary Fund, in its April 2026 World Economic Outlook, pointed out that due to factors such as the Middle East war, global economic growth is expected to slow to 3.1% in 2026 and 3.2% in 2027, with downside risks still dominating—challenges such as geopolitical fragmentation, trade frictions, and financial volatility remain.

However, the absence of risk does not equate to the absence of opportunity. For observers, a more noteworthy change is that as extreme uncertainty begins to ease marginally, and as risks gradually shift from "unpredictable" to "manageable," market expectations, policy pace, and liquidity structure often react first.

Xin Ding Sheng believes that as the cyclical adjustment nears its end, the market will not immediately show a full recovery. However, liquidity recovery, marginal policy changes, and improved industry expectations are often the most genuine leading signals of a new cycle. Every adjustment is the prelude to a new cycle; every market downturn may be accumulating strength for the next trend.

Mr. Chen emphasizes that Sino-US relations will not simply move towards a full easing, nor will short-term competition be eliminated immediately. A more realistic path is that capital, technology, and supply chains will find a new balance point in the new normal of "competing, cooperating, and managing risks simultaneously."

The key significance of this change for the market lies in the fact that the pricing logic of risk is changing. In periods of high uncertainty, capital naturally tends towards risk aversion, amplifying market reactions to external shocks. Sectors such as technology manufacturing and cross-border supply chains are prone to valuation suppression. However, as risks gradually become more manageable and predictable, the market may reassess ecosystem nodes with long-term industrial value. This does not mean all risks will disappear, nor does it mean the market will immediately enter a one-sided upward cycle. On the contrary, the new market environment is more likely to exhibit characteristics of "slow recovery, structural differentiation, and liquidity reallocation."

The World Bank, in its January 2026 Global Economic Prospects report, pointed out that despite persistent trade tensions and policy uncertainty, the global economy has shown some resilience, with global growth projected at 2.6% in 2026 and rising to 2.7% in 2027. However, if this forecast materializes, the 2020s could still be the weakest decade of global growth since the 1960s.

This means that future market opportunities will not come from a simple, comprehensive recovery, but more likely from structural repair and industrial value reassessment. With market recovery signals, liquidity opportunities may be re-stratified. Every market correction, while superficially a price fluctuation, is at a deeper level a rebalancing of expectations, liquidity, and fundamentals.

During periods of market uncertainty, funds typically favor defensive positions, risk appetite declines, and many industries with long-term value are temporarily undervalued. However, when policy expectations gradually stabilize, external risks ease marginally, and financial conditions improve, capital often prioritizes seeking new structural opportunities.

The IMF, in its January 2026 outlook, noted that technology investment, fiscal and monetary support, relatively loose financial conditions, and the resilience of the private sector are, to some extent, offsetting the pressures from changes in trade policy and uncertainty.

Future liquidity opportunities will not be evenly distributed but are more likely to concentrate in the following three types of ecosystem nodes:

First, industries with policy-supported logic.

For example, sectors such as technology manufacturing, smart infrastructure, energy systems, and supply chain security are more aligned with the macroeconomic themes of stabilizing growth, stabilizing expectations, and stabilizing the supply chain, and are more likely to receive long-term resource support.

Second, high-quality ecosystem pillars with genuine industrial value.

Market recovery will not reward mere conceptual hype in the long run, but will focus more on technological barriers, commercialization capabilities, cash flow resilience, and the real ability to implement industrial projects. Those roles that can prove their "usefulness" during fluctuations are the nodes worth long-term commitment.

Industry chain collaboration nodes with cross-cycle adaptability.

Against the backdrop of global relationship rebalancing, cross-border industry chains will not simply decouple, but will enter a more compliant, regionalized, and refined restructuring phase. Nodes that can bridge different rule systems and collaborate across different markets will gain stronger vitality.

From the perspective of an ecosystem observer, market recovery does not equate to risk clearing, but rather signifies the formation of a new allocation framework. The next stage of forward-looking planning should revolve around three main themes: stable growth, stable expectations, and stable industry chains.

Stable growth means that policies and resources are refocusing on the real economy.

Against the backdrop of global growth pressure, policymakers need to enhance the resilience of the real economy through technological manufacturing, infrastructure upgrades, energy synergy, and substantial empowerment at the industrial level. The more vital sectors for the future lie in those capable of driving industrial upgrading, improving production efficiency, and generating long-term growth.

Stable expectations are a prerequisite for the recovery of market risk appetite.

As expectations of extreme confrontation in Sino-US relations shift towards risk management, capital markets' assessments of cross-border trade, technological cooperation, and supply chain stability are expected to improve. Once expectations improve marginally, those high-quality industrial nodes that have been suppressed for a long time may see a rediscovery of their value.

Stable industrial chains are the core of future structural opportunities.

Global supply chains will not return to the past model of prioritizing efficiency alone, nor will they simply move towards complete decoupling. What is more likely to emerge is regional collaboration, compliance management, diversified layout, and strengthening of key links. Companies with supply chain organization capabilities, cross-border resource integration capabilities, and risk management capabilities will be more likely to gain a competitive advantage in the new cycle.

Without liquidity, industry value may be undervalued in the long term; without trend, market enthusiasm is often unsustainable. The truly noteworthy window often appears at the intersection of clear industry trends, marginal improvement in liquidity, and the beginning of market expectation recovery.

From a trend perspective, technology manufacturing, AI computing infrastructure, new energy systems, cross-border industrial chains, intelligent manufacturing, and the digital economy remain core areas of global industrial competition.

From a liquidity perspective, as policies place greater emphasis on stabilizing growth and expectations, capital market risk appetite is expected to gradually recover, and high-quality industrial assets may re-enter the resource market's focus.

From an industry perspective, supply chains will not simply decouple but will be re-stratified, reorganized, and reallocated through competition and cooperation.

The combination of these three factors constitutes a crucial window to watch in the next stage of market recovery.

Therefore, SHINDEV believes that the current focus should not be solely on short-term market rebounds but rather on the underlying trend logic of liquidity recovery. What truly matters is not when market sentiment fully recovers, but which industry sectors have begun to have the foundation for repricing.

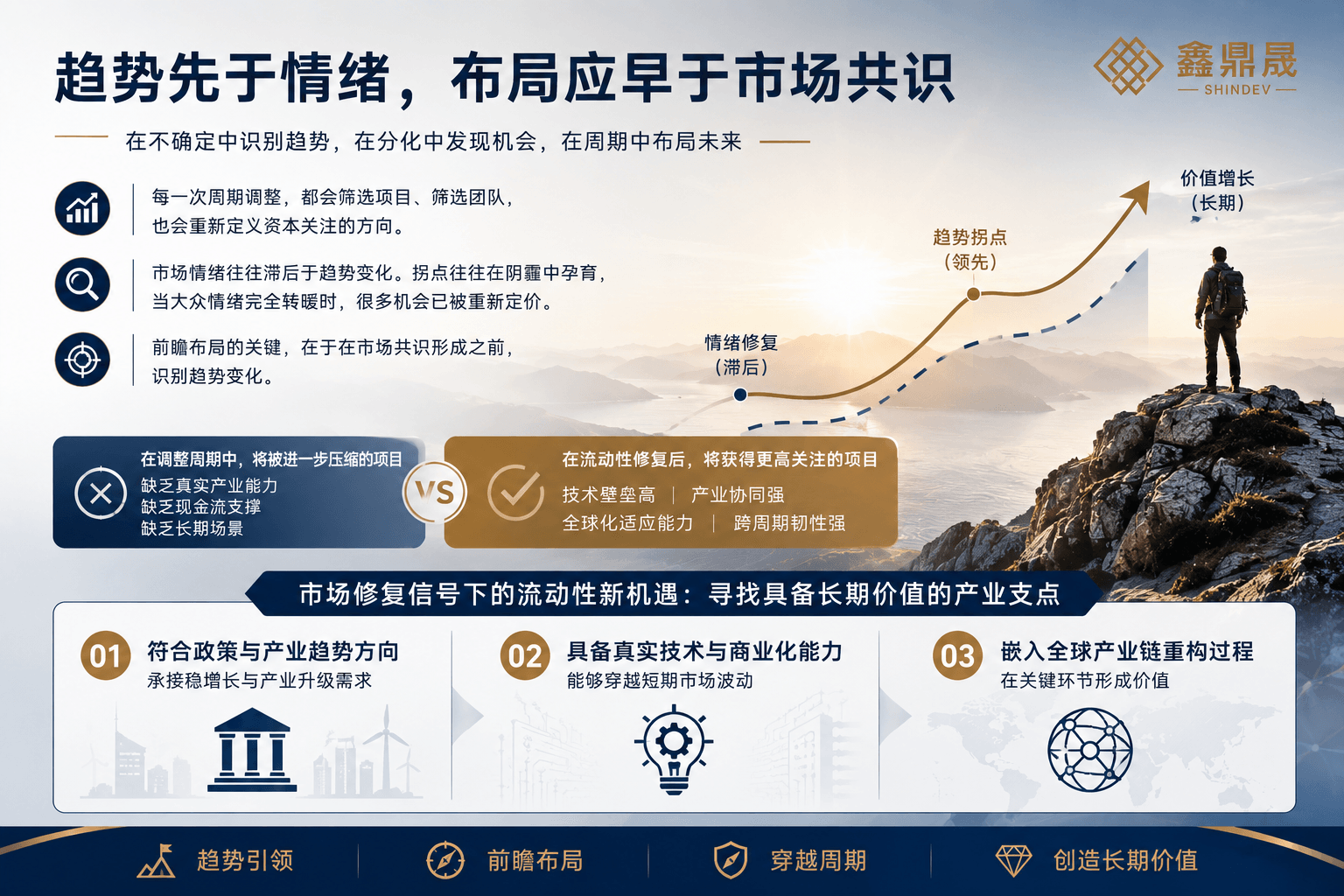

Every cyclical adjustment filters out those lacking genuine capabilities and redefines the focus of resources. Market sentiment often lags behind trend changes. While the market remains gloomy, a true industry turning point may already be emerging; by the time public sentiment fully recovers, many opportunities have already been repriced. The key to forward-looking positioning is identifying trend shifts before market consensus forms.

During adjustment cycles, those lacking genuine industry capabilities, cash flow support, and long-term application scenarios may be further marginalized; while ecosystem nodes possessing technological barriers, industry synergy capabilities, global adaptability, and cross-cycle resilience have the opportunity to gain greater attention after liquidity recovers.

Therefore, new liquidity opportunities arising from market recovery signals are not simply about chasing rebounds, but about finding industry pillars with long-term value during cyclical adjustments.

These types of industry pivots typically possess three characteristics:

1. They align with policy and industry trends, capable of meeting the genuine needs of stable growth and industrial upgrading;

2. They possess genuine technological and commercialization capabilities, enabling them to weather short-term market fluctuations;

3. They can be embedded in the global industrial chain restructuring process, forming irreplaceable node value in regional collaboration, cross-border services, energy infrastructure, or technology manufacturing.

From the perspective of ecosystem co-builders, liquidity release itself does not necessarily bring high-quality opportunities. What truly deserves attention is: how liquidity will choose its direction, how it will repric assets, and how it will empower truly vibrant industry pivots.

In past cycles, the market has given extremely high valuations to high-growth narratives. However, in this new phase, resources will place greater emphasis on certainty, efficiency, resilience, and genuine industry value. This means that future ecosystem pivots need to answer three core questions:

1. Can they maintain growth resilience amidst macroeconomic uncertainty?

2. Can they find a clear position within policy and industry trends?

3. Can the market absorb the reallocation of resources and capabilities after liquidity recovery?

Against the backdrop of global relationship rebalancing, strengthened risk management mechanisms, and gradually stabilizing policy expectations, these areas may become more noteworthy structural directions in the next phase of market recovery. Technology manufacturing, energy synergy, AI infrastructure, cross-border industrial chains, and intelligent upgrading are precisely the convergence points of these issues.

As an ecosystem co-builder that continuously focuses on technological innovation, intelligent infrastructure, and industrial upgrading, SHINDEV believes that market recovery does not mean the end of risks, but rather that new value judgments are forming.

In the future, SHINDEV will continue to focus on the three main themes of "stabilizing growth, stabilizing expectations, and stabilizing industrial chains," paying attention to structural opportunities in technology manufacturing, AI computing infrastructure, new energy, cross-border industrial chains, and high-growth ecosystem nodes, and is committed to providing deep empowerment and long-term support to these nodes.

Based on CEO Chen Rui's previous judgment of "from combating expectations to risk management," the global market is entering a new stage that places greater emphasis on expectation recovery, liquidity revaluation, and the rediscovery of industry value. The macroeconomic environment doesn't directly create long-term value, but it alters the path in which value is discovered, priced, and amplified. As the market shifts from extreme uncertainty to risk management, as liquidity moves from contraction to marginal recovery, and as policy shifts from risk prevention to growth stabilization, those ecosystem nodes with genuine long-term competitiveness will have the opportunity to reclaim center stage.

Every adjustment is the prelude to a new cycle.

Every period of uncertainty is a process of accumulating strength for a trend.

Trends precede sentiment, and strategic planning precedes consensus.

In this new market cycle, SHINDEV will continue to adopt a long-term perspective, seizing structural opportunities arising from the rebalancing of global relations and the restructuring of industrial chains. We will promote more efficient connections and synergies between capital, technology, and industrial resources, building a more solid foundation for the growth and value release of future high-quality ecosystem nodes.